You could save thousands on dispensary insurance costs by understanding how premium is calculated

Table of Contents

We’ve written about the cost of cannabis insurance before. This time we take a real example of a client who switched their pricing structure and ended up saving a lot of money on their cannabis insurance. The dispensary insurance costs are based on what factors the insurance company uses to price the operation.

There are two pricing factors used by cannabis insurance companies:

- Revenue or

- Square footage

Revenue is the total amount of sales being projected for the upcoming term before costs of good sold and operating expenses. Those sales will include everything being sold at the store such as flower, edibles, concentrates, accessories, paraphernalia, etc….

Square footage is also known as “area”. Square footage is based on the size of dispensary being occupied based on the length and width in feet multiplied by each other. The price difference between the two is significant with one strategy being the clear winner.

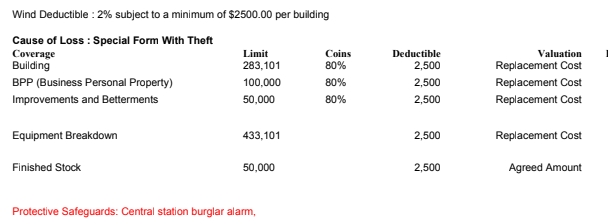

It should be noted this article applies specifically to the general liability insurance product. Cannabis business property insurance is always calculated on a set pricing factor not based on revenue or square footage. Product liability insurance is priced on revenue by most if not all insurance companies.

Dispensary insurance cost based on revenue

To calculate the insurance premium based on revenue, the insurance company uses the total projected revenue for the year and multiplies it by a factor.

For example:

| Revenue: $3,700,000 |

| Pricing Factor: $.0010875 |

| Premium: $4,024.00 ($3,700,000 * $.0010875) |

In the example, the cannabis store had revenue of $3,700,000. The insurance carrier will multiply the revenue by their pricing factor of $.0010875 to determine the annual premium of $4,204.

Dispensary insurance cost based on square footage

The cannabis insurance company that uses square footage is taking the amount of space occupied by the store or dispensary and multiplies by a factor. For example:

| Square Footage (length times width in feet): 4,500 |

| Final Rate: .076 |

| Premium: $342.00 (4,500 * .076) |

The dispensary insurance cost is calculated by the square feet of 4,500 times the pricing factor of .076. The annual premium for general liability is $342.00.

Dispensary insurance cost based on revenue could be 120% more expensive

The above examples are from a real client located in Colorado. The clear winner is the insurance carrier that rates on area will save that dispensary $3,682 per year. Remember, this calculation is just general liability insurance and does not include any business property insurance such as cannabis stock, equipment, cash, loss of income, etc….

{kind=link}

When to change your dispensary insurance if your costs are based on revenue

The idea time to change your cannabis dispensary insurance is when your policy renews. All cannabis insurance policies are based on a one year term. A review of the dispensary insurance policy will show those dates.

If the policy is not close to expiring, then it might make sense to terminate your coverage depending on if your past what is known as 25% minimum earned premium. Anytime a dispensary begins a new insurance policy, the cannabis insurance companies will state on the quote it is subject to a 25% minimum earned premium charge. This means canceling early in the term will cost you this amount. Once your beyond this period of time (about 3 months), then it could be safe to terminate coverage.

Saving dispensary insurance costs for general liability means finding the right insurance company and broker

If you are searching to save money on your cannabis insurance, you will need to find a broker who has access to the few insurance companies that price polices on revenue for their general liability. This dispensary client saved $3,682 per year because the insurance company priced the insurance on square footage as opposed to revenue.

This is a significant savings!