Regulations and Insurance: Understanding the Regulatory Requirement

Table of Contents

New Jersey cannabis retailers and stores may be adding delivery service to meet the needs of their customers to increase sales and provide an alternative purchasing alternative. This was the result of the Cannabis Regulatory Commission approving N.J. Admin. Code § 17:30-14.8 – Home delivery.

The regulations are below:

Home-Delivery-Guidance-Document-12.1.23“(r) A cannabis retailer and cannabis delivery service shall maintain current hired and non-owned automobile liability insurance sufficient to insure each delivery vehicle in the amount of at least $ 1,000,000 per occurrence or accident.”

N.J. Admin. Code § 17:30-14.8

Understanding Hired and Non-Owned Auto Liability to meet NJ’s Requirement

Within these regulations, a specific type of cannabis insurance coverage named “hired and non-owned automobile” or “HNOA” must be purchased by both the dispensary and delivery licensee. Essentially, the hired can mean any vehicle you lease, hire, rent, or borrow. Non-owned auto can mean any auto your do not own, lease, hire, rent, or borrow. Both of these terms are defined by the insurance policy.

Renting a car or hiring a delivery service

Some simple examples would be renting a car could be deemed hired auto and non-owned auto is a personal vehicle driven by an employee.

Before we go further, let’s discuss what are the risks from New Jersey cannabis stores making deliveries to their customers and what cannabis insurance should be considered.

Cannabis Delivery Risk to Think Through Carefully

There are several risks for store owners to consider. This article will not discuss certain risks associated with protecting the cannabis stock or property such as theft or damage from an accident. However, the store owner should consider cannabis insurance for stock being covered during transportation.

Risk #1: At fault accident by store employee

The first risk involves a store vehicle causing an at-fault accident injuring another party along with property damage. The vehicles primary insurance is important when this happens. The cannabis insurance HNOA becomes just as important providing additional liability protection to the store.

Risk #2: Failure to secure the right type of insurance leads to a statutory violation

The second risk may be statutorily non-compliant because the cannabis insurance HNOA product is the wrong type. The due diligence when buying cannabis insurance HNOA become important when buying the right coverage.

Risk #3: Store relies on a third party to make deliveries

A third risk could be if a store is relying on another party to make deliveries on their behalf. The vehicles primary insurance is important when this happens. The cannabis insurance HNOA becomes just as important.

Your cannabis insurance general liability carrier will not cover this type of risk.

Cannabis insurance general liability is frequently purchased by cannabis companies. This coverage is primarily meant to cover certain risks from the premise. Cannabis insurance companies will offer and add HNOA by request as a separate line of coverage. Again, by request and separate line of coverage and becomes part of the general liability insurance product as a separate coverage line.

If a store owner purchases HNOA through their general liability cannabis insurance carrier, they must understand the intention of the coverage is usually for incidental use and not meant to be used for delivery service. An example of incidental use would be having an employee driver their vehicle to the bank, post office, or supplies. The cannabis insurance carrier(s) do not want this coverage to be used for delivery service.

If you are relying on this coverage to meet the statutory requirements for delivery service, you could be placing your company at risk if an accident were to occur.

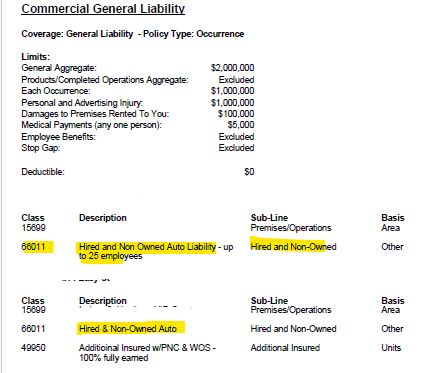

What to look for on a Hired and Non-Owned Auto Liability Quote

Below is a quote from a cannabis insurance company. In yellow, the Hired and Non-Owned Auto Liability is being added to the coverage. The carrier utilizes specific class codes and description.

A condition of the coverage is stated by the insurance company on the quote below. Errands such as a trip to a post office or purchasing of supplies are acceptable forms of risk. Ironically, the insurance policy does not condition this requirement within the policy. This may create uncertainty if a claim were to occur since the quote states the requirement, while the policy does not. This will ultimate be left to the courts to decide.

Cannabis Dispensary Insurance Cost for HNOA

The bottom line for New Jersey cannabis stores who’ve bought cannabis insurance hired and non-owned auto from their primary general liability insurance carrier for the purpose of covering a delivery service is no coverage exists.

Meeting NJ’s Cannabis Delivery Insurance through a separate policy

This means they will need to buy a separate policy to cover cannabis insurance for HNOA. The dispensary insurance costs will typically start at $7,500 per year. This dispensary insurance cost is significantly more expensive than adding HNOA on the existing general liability insurance policy.

Need to buy cannabis insurance for delivery?

IF you need this special type of insurance to meet NJ home delivery regulation between visit our contact page. We will get back to you as soon as possible.