Reducing the Price of Cannabis Business Insurance without hurting your company

Table of Contents

Today, many cannabis companies are looking to reduce their costs in order to save money. Insurance happens to be one of the expenses that can add up between general liability, property, workers compensation, product liability, and directors & officers insurance.

Tip #1: The Price of General Liability Insurance based on revenue could cost more

General liability is one of the more important coverage lines covering essentially your premise. Depending on the insurance company, your price might be determined by either square footage or revenue. We believe a store rated on square footage is more cost effective because the size of your location remains unchanged. Revenue will fluctuate. As the revenue increases, the premium will correspondingly increase.

Another important factor is insurance companies who don’t use square feet as a pricing factor, will not audit your financials. This saves time and money from having to provide documents to the carrier in order to substantiate your revenue. If for example you estimated your revenue at $1,000,000 for the year. After the insurance company conducts their audit, the revenue was $2,000,000, then you will receive an invoice for the difference.

If you are a grower or manufacturer, then most cannabis insurance companies should rate your facility based on square footage. However, if you have a quote or current insurance rated on revenue, then find an insurance broker to help you with a square footage based policy to save you time and money.

Tip #2: Saving on Price by removing cannabis stock due to strict requirements?

Cannabis insurance companies have requirements when you are seeking coverage for cannabis stock. These requirements typically involve specifications for your safe along with central station alarms, video cameras, and motion detectors. If you know your insurance carrier requires an 800 to 2,000 pound safe bolted to the ground, then buying the cannabis stock coverage might not be the best use of your premium dollars. Depending on a variety of factors, cannabis stock coverage can cost $1.00 per $1,000 of coverage. A $100,000 of cannabis stock coverage may cost at least $1,000 per year. If your safe isn’t compliant, then the carrier might deny a claim for theft.

What if the claim doesn’t involve theft when you have a non-compliant safe? This situation depends on the insurance carrier if they’ll cover a loss for fire as an example. If the insurance carrier is “all or nothing,” meaning the safe must be compliant for any type of claim to be covered, then you might be better off saving the $1,000 in the example above by eliminating the coverage.

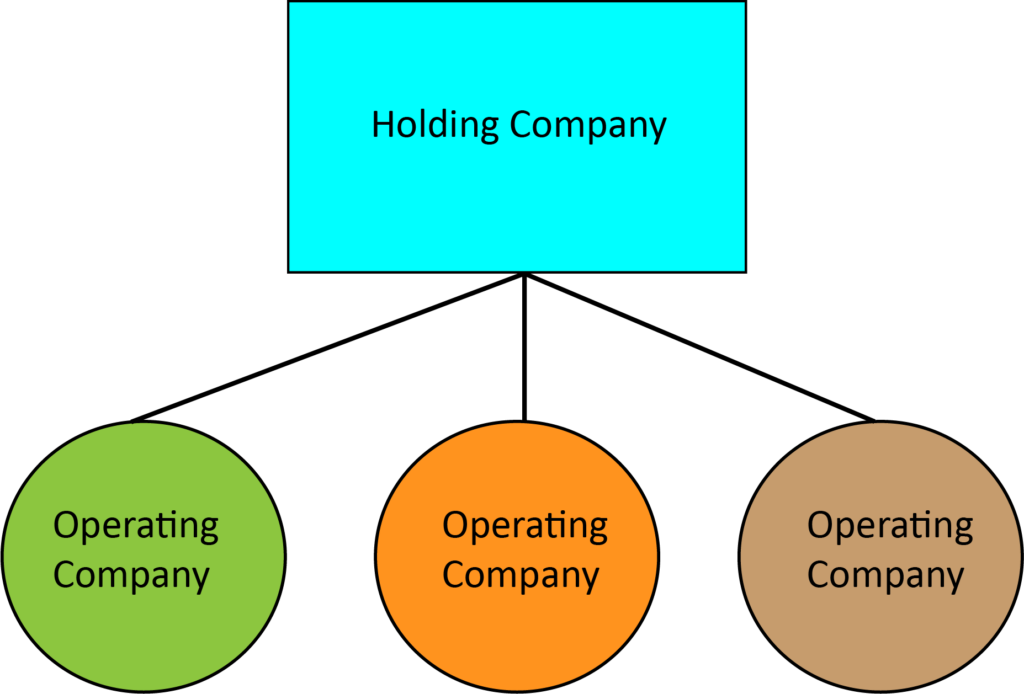

Tip #3: Consolidate holding and operating companies on one policy

If your cannabis operation has a holding company and perhaps multiple operating companies with common ownership, then it could make sense to consolidate all of the entities on to one policy. Typically, the key to this cost saving strategy is the ownership must be commonly owned entities.

If the holding company is owned 50% by Owner A, and 50% by Owner B, and the operating company has identical ownership, this would meet the requirements. However, if the operating company is ownership is Owner A 25%, Owner B 25%, Owner C 25%, and Owner D 25%, then this might not meet the threshold for common ownership. The reason insurance premiums are reduced by consolidating on one policy is because fees are charged by the policy.

The disadvantage to consolidating your insurance with this cost reducing strategy are liability limits are shared amongst the companies. The holding and operating companies all share the same limits essentially reducing the amount of coverage. The other disadvantage is if one operating company is liable in a claim, then the claim history impacts the entire family of companies.

Tip #4: Growers with LED lighting will have more access to insurance companies and save money

The cannabis insurance industry will reward cultivators who operate with LED grow lights with more options and favorable pricing. The severity of grow fires from exploding HID bulbs has been a common problem and underwriting concern for several years. Not only will you save money on your cannabis insurance, but these lighting systems will reduce your operating costs on electricity improving your profit and loss.

Tip #5: Spend your insurance premium on equipment breakdown and coverage extensions

Equipment breakdown is a property coverage that provides inexpensive insurance for your business property due to an accident that leads to a mechanical breakdown, electrical disturbances, and other perils. Typically the price for this coverage is about 8 percent of the cost of covering business personal property.

For example, insuring $850,000 of business property would cost $3,655 per year. Insuring the same $850,000 for equipment breakdown is $263.00 per year. This is not a cost saving strategy, but rather a coverage provision that provides value to your overall insurance protection. If you are going to insure your business property, it makes sense to add this coverage because its not expensive.

This blog has written about coverage extensions here. Essentially, these are additional coverages such as money, sewer back up, employee dishonesty, etc…. Insurance carriers will offer specific limits such as $10,000, $25,000, $50,000, or $100,000.

There are two primary reasons to include this coverage are (1.) its inexpensive and 2. there are less requirements for cash to be covered. According to published study through The National Association of Insurance Commissioners 70 percent of cannabis companies operate as a cash only business. This means cannabis companies are holding on to a lot of cash with no bank to safely guard it. Let’s face it, insurance companies will not make it easy to collect from them on a claim. Depending on the insurance carrier, this is one coverage extension that should be seriously considered because there are less barriers to overcome. The cash and employee dishonesty coverage alone is worth adding this your insurance.

If you are looking to implement any of these cost saving strategies, please complete our online application for cannabis insurance to get you started today.